Insurance Doctors Expect™

Doctors value disability insurance, but they often can’t find the right type or amount of coverage, resulting in a coverage gap. MGIS disability insurance coverages solve these challenges for doctors.

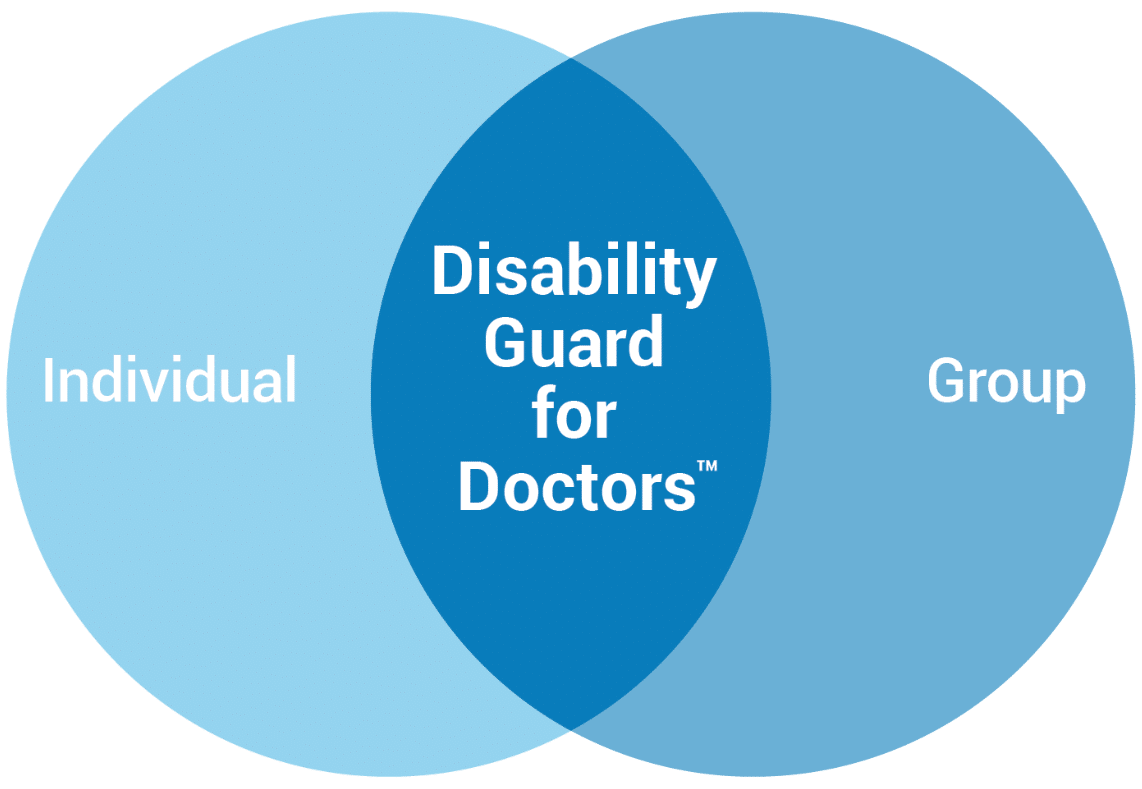

Disability Guard for Doctors™

Disability Guard for Doctors™ uniquely combines the best coverage features of individual disability insurance with the cost and underwriting advantages of group insurance.

High Limits Disability Insurance

Some high-earning doctors may still face an income-protection gap even with individual and group coverage in place. MGIS High Limits Disability Insurance adds another layer to help doctors enjoy up to 70% income replacement.

MGIS disability insurance solutions work together to reduce income replacement gaps

Learn how Disability Guard for Doctors™ can complement your individual coverage and how our High Limits Disability Insurance plan can solve your income gap up to 70%.

Helping You Succeed

MGIS works with select insurance brokers to deliver the very best disability insurance to doctors nationwide, including all medical specialties and all practice settings.

We’re excited to carry our decades-long legacy forward, driven by executive and broker leadership who bring advanced industry expertise. We offer the foresight to anticipate income protection and specialized insurance needs while helping partners adapt within a constantly evolving healthcare environment—delivering not only the right amount but also the right type of insurance coverage.

Contact us to learn more. Call 800.969.6447 or visit our contact page.